Call Us: 972-724-2881

This is the start of a America's very best newsletter-blog for everything to do with Divorce and Mortgage Financing. We offer the divorcing community across America a clear, comprehensive, authoritative answer to every conceivable question that divorcing folks (and family law professionals like lawyers, financial planners, realtors, etc.) have concerning a very specific niche – the intersection of Divorce and Mortgage Finance.

This is the first blog-article; and, I promise that if you take the time to read my material you will absolutely get value from it. There will always be useful information. This is not some idle, fanciful hope. I've done it for years with family law attorneys. And, I've kept that promise. If any attorney opens my email, they will always find usable information for their practice of family law, specifically how Divorce affects – and is affected by – Mortgage Financing.

It's a huge set of problems and issues. And, most people only face them once in their lifetime, if that much. (Although, most of us know many couples who get divorced and could use some solid information about what they can and can't do regarding home ownership and financing). But, it involves, for most people, is the biggest asset they own – their residence.

Just because this is introductory doesn't mean I will not give you some "solid meat." In fact, you may come back to read this article or pass it on to friends many times. I am going to show you how divorce affects your ability to own a home, buy a home, finance a home...and – MOST IMPORTANTLY – what you can do to control the situation.

You do not have to be a victim when it comes to owning your home and getting the best financing possible. You just have to know the rules. And, it helps to be hooked up with knowledgeable Divorce-Lending Specialists. The bad news is that there are not very many of them. The good news is – I know a guy. 😊

So, I read Content Marketing by Jim Pullizzo and he told of a guy who started a very successful blog about pools by writing out every question he could think of that folks have about pools.

So, I sat down and began writing as many questions as I could think of, everything I remembered people asking me, everything attorneys had asked me that I could re-phrase to be a question from a divorcing person.

Then I put it out on Instagram – what questions, I asked, would you have about divorce and mortgage finance. The first response I received was from a helpful friend of mine and my sons, Zach Ross. I had met Zach a few years ago. He is a young entrepreneur with an infectious attitude and a warmth that endeared me to him. His question was perfect. Thanks Zach for getting me started off right.

Zach responded: So, divorce affects your ability to get a mortgage?

So basic. Since I lived, breathed, ate and drank it for the better part of 20 years, I took for granted that everyone knew it.

ABSOLUTELY, a divorce affects your mortgage financing.

A divorce ABSOLUTELY affects everything about your mortgage and your home ownership. The divorce decree is an outline of your life. It reveals how much you owe and how much you receive in income and what assets you receive or part with.

So, when a mortgage lender is deciding whether or not to lend you money, they will look at YOUR LIFE – especially everything with a dollar mark - $ - beside it and everything with a number attached to it. The lender will take note of timing issues to determine whether or not your support income can be counted as "qualifying" income.

That is, how long you receive child support or alimony or spousal support – well, it's revealed in a divorce decree. How much you have to pay and for how long you have to pay it – that's also revealed in a divorce decree.

Now here's what very few people understand. And, when I say "people" what I mean is "ALL PEEPS." Lawyers, judges, mediators, folks who are divorcing, financial planners, realtors, and YES – even mortgage professionals.

The divorce settlement can either accommodate your mortgage loan approval or totally sabotage it.

I don't just point out the potential pitfalls and liabilities in a divorce decree. I consult with the divorcing party and their attorney to make sure those pitfalls and disqualifying features of a settlement are AVOIDED.

So, what's the take-away in this introductory message about your divorce settlement? It's very simple – you need the services of an experienced Divorce-Lending Specialist. That's going to be the take-away for every issue imaginable – get the expert on it!

Here's why. One of our trained specialists will know how to pre-underwrite your divorce settlement AND make recommendations for the precise language that is required in the final decree to make sure your loan will be approved. Pre-Underwriting is very important. But, it IS counter-intuitive to the mass of the mortgage industry. Nobody expects it. Not yet anyway. One day, it will be standard operating procedure. But for now, it's unique and unusual.

We do it. And we do it right.

We use what we call the Wayne Gretzky Method. Gretzky is the famous hockey player who, when asked the secret of his scoring record replied "I always skate to where the puck is going to be, not to where it is." That's what we do. We also think of it as reverse engineering. We project into the future – we determine what you need the end result to be – and then we "reverse engineer," working backwards to design your loan intentionally.

Things to keep in mind.

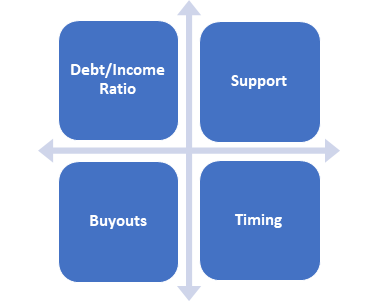

So, here's a peek at the Four Make-Or-Break Factors in a Divorce Settlement that Absolutely Affect Your Ability to Get a Mortgage Loan.

Any one of these issues can become a problem which can become a disqualifying factor in your mortgage loan.

You know that the first key is to solve the issues in advance by applying now with a qualified Divorce-Lending Specialist

Now, watch the next video and read the next blog to learn what the first Make-Or-Break issue in your divorce settlement.